A question we often get is, “Are there real High-Frequency Trading opportunities in Crypto?”

High-frequency trading implies that there are opportunities in the market to make fast, quick trades in order to capture small mispricing opportunities in-market. These pricing opportunities might be caused by a host of reasons including latency in pricing signals, or disparity between different markets and exchanges.

For these reasons, HFT requires a high degree of automation and speed to find and execute on opportunities.

However, it also requires a high degree of capacity and liquidity. While there may be momentary mispricings in every market, to build a robust high-frequency trading algorithm and execution set, you need for there to be enough market volume (or ‘capacity’) to take advantage of that.

That’s because, even if you can find a coin mismatched for a fraction of a percent, the lack of capacity will drive the price away from the market rate, and the price will move. That eliminates the high-frequency trading opportunity. In short, HFT opportunities require advanced techniques to identify trading opportunities, speed to execute on those short-lived pricing opportunities, and critically, market capacity.

In crypto markets, those short-lived mispricings rarely find their way, in any scale to the general public. The price mismatch can be identified at the point of ‘exchange’ and is often captured in micro parts by ‘whales’. Those whales have unique placement and visibility to capture whatever limited opportunities there are for arbitrage.

High-Frequency Trading in Crypto and the “Capacity Challenge”

When trading companies approach the question of capacity, the main concern is that certain algorithms work in certain trading niche areas, and inherently will experience a bottleneck that when reached becomes less profitable.

As an example, within high-frequency or arbitrage-style trading, the bottleneck is the number of short-term opportunities within both the market and the available volume of level 2 books. Once participants close the spreads and differences between exchanges, the profitability goes down significantly.

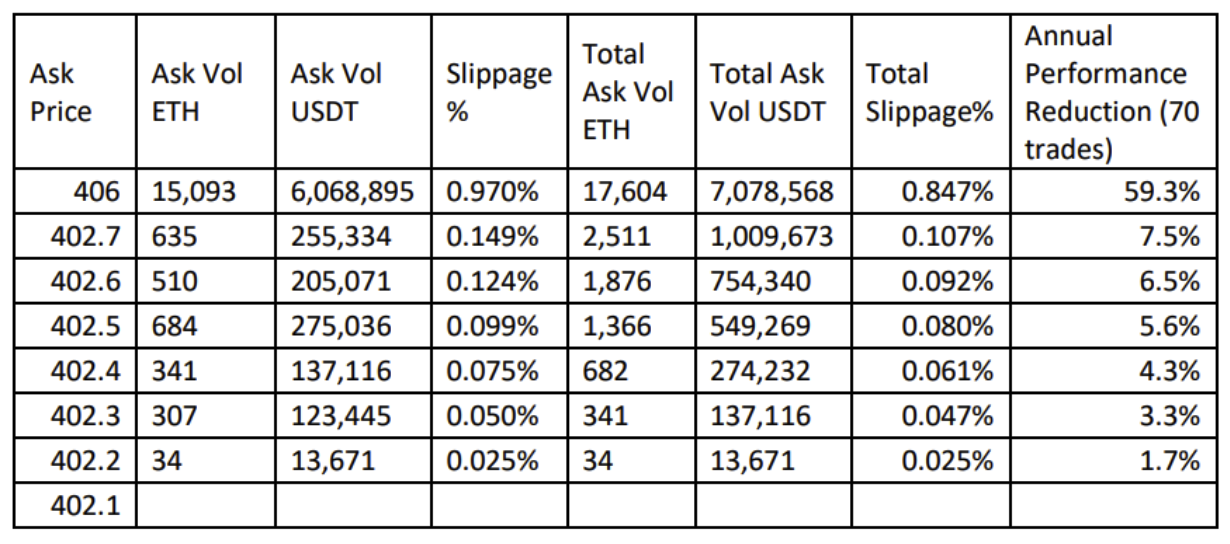

EndoTech’s trading style is a long-term approach to trading. Each strategy makes 20 to 70 trades per year. Our capacity relies primarily on slippage – the difference between where the strategy signaled the entry and exit for each trade and where actual order was executed.

For example, in the case where you have an automated strategy that:

- The performance showed an “on paper” return of 250% annually,

- It did 70 trades that year,

- Each trade experienced average slippage of 0.65%

We see that the slippage of execution eliminates most of the theoretical performance gains. In this case the actual ‘money performance’ on that account will show 250%-[70*0.65%]=104.5%.

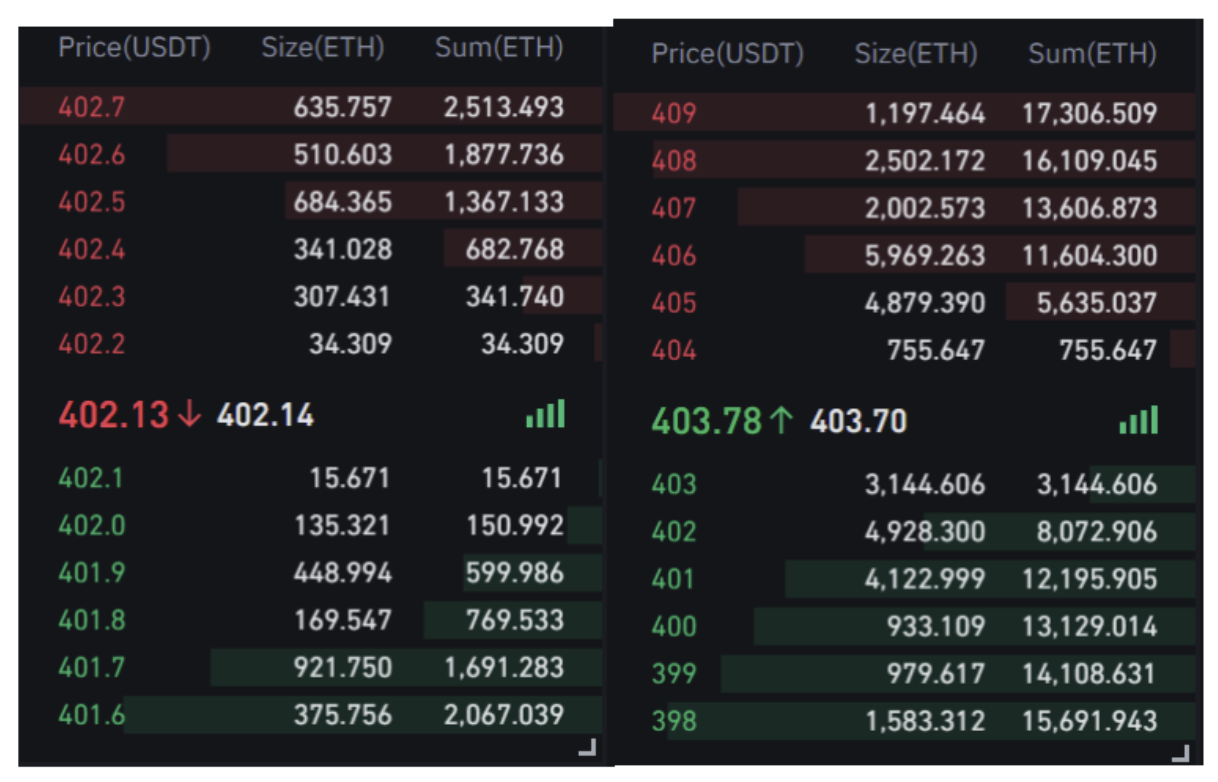

One of the straightforward ways to predict slippage is to use a level 2 book, here is an example:

Example of Binance Futures ETH/USDT level 2 book

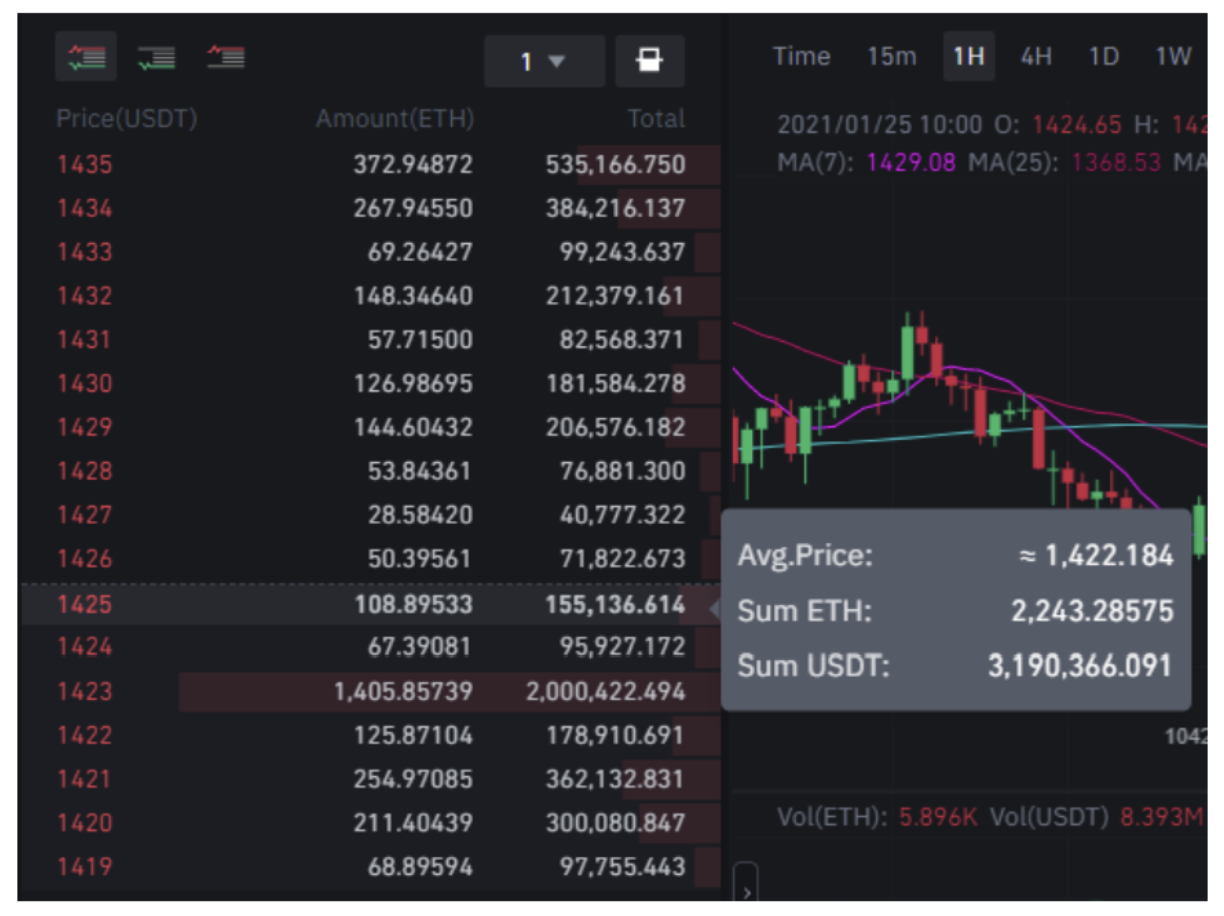

Finally, the crypto market continues to experience high volumes and further improved the volumes and slippage – see next figure.

Example of Binance Futures ETH/USDT level 2 book

In conclusion, for fixed capital trading portfolios with 250% in ‘paper’ annual profits for a portfolio volume of $480M across Binance Futures, Coinbase, and Gemini exchanges with $3M of each ETHUSDT single trade size, will lose up to 0.2% in slippage. The net result of this lack of capacity will be that the 250% profit, results in a total loss of 28%!

While high-frequency trading implies the ability to execute many trades quickly to capture mispricing. The Crypto market is not yet as liquid as necessary to capture these slight price movements at scale. As a result, any arbitrage opportunities are captured by ‘whales’ or are lost at volume.

EndoTech and High-Frequency Trading and Capacity

EndoTech’s portfolio consists of 40 strategies that run on ETH, BTC, and top 11 altcoins. Our expected reduction due to increased AUM will be in trading ETHUSD(C/T/B) since BTC slippage for 500M size trades is still under 0.2% in Binance, Coinbase, Gemini, etc.

Avoiding The Breakouts

An additional consideration is that EndoTech algorithms typically do not enter during breakout moves. In 85% of the entries, EndoTech algorithms enter prior to the moves, meaning that our TWAP methodology allows us to enter for 4 hours every 10 minutes, without affecting the market. And our exits are happening PRIOR to trend move completion, thus limit orders are not suffering ANY slippage.

For example, since ETH allocation is 45% of the total portfolio, one can assume a total estimated portfolio P&L of 237%.

Real Results

That means that a portfolio goal of $480M with a maximal expected reduction on performance is: an annual profit of 250% will resolve to 237%

To resolve the next level of portfolio AUM – we will need to see significantly more liquidity or diversify into OTC solutions that offer fixed 0.65%-0.85% in spreads (no slippage), and optimize it between all the OEM pools.

Capacity Planning

If a company cannot solve capacity issues it will not survive at scale.

EndoTech’s methodology is to know up front where and when such capacity issues can hit. The algorithmic team is developing tools in advance to manage these capacity issues. The team also understands that it is the real results that win adoring customers – not ‘theoretical’ and ‘backtested’ results.

EndoTech’s team has created a capacity-based execution engine and is cognizant and communicative of the opportunities and limitations of high-frequency trading in cryptocurrency.